Dempster Mills Manufacturing Company

A Classic Turnaround Story

Long before becoming the “Oracle of Omaha”, Warren Buffett sometimes pursued private equity-type deals: buy undervalued businesses, improve business operations, and sell for a profit. Buffett’s investment in Dempster Mills Manufacturing Company (Dempster) is a compelling example on how to turn around a struggling business in a declining industry.

He started buying the stock of Dempster in 1956, early in the years of his investment fund. It was originally a classic “cigar butt” play. The initially stock price was $18, much lower than the $72 book value. Eventually he would buy enough shares to gain control of the business. Although he did not set out to gain control, he was not afraid to take a more active role in realizing value for the business.

Background

Dempster was renowned for its windmills and farming equipment in the Midwest for decades, but new technologies such as electric pumps and engines cast a grim shadow over the company’s future. Sales stagnated and the stock price plummeted. Excess windmills sat unsold, receivables were not collected from struggling farms, and the company needed to invest in new equipment for future production at even higher costs. As a major employer in Beatrice, the company’s financial health had major influence on the local community.

Buffett and Munger both warned about asset-heavy businesses. In his 1983 letter, Buffett wrote that such businesses generate low returns, “barely providing capital to fund the existing businesses and have little room for growth.” Munger said in 2003 that he hates business where hard assets tie up the profits instead of free cash.

Could such a business like Dempster still be a worthwhile investment opportunity?

Buffett’s Involvement

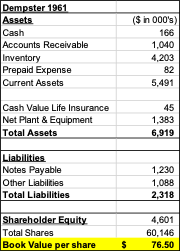

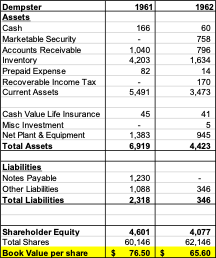

Buffett gradually increased his ownership of Dempster over the years, owning 71.7% at an average price of $28 per share. Such price was well below the $76 book value in 1961. Dempster ended up 21% of the Partnership portfolio, which signaled a major shift from his “generals” strategy of passive value investing to pursuing active control.

Buffett emphasized in his 1963 letter that, “when control of a company is obtained, obviously what then becomes all-important is the value of assets, not the market quotation for a piece of paper.”

It was Buffett’s first direct involvement in a business, leading him to become the company’s chairman. His actions indicate his thorough research and patient buying. More importantly it illustrated his willingness to bridge the gap between the stock price and intrinsic value directly, when the market did not. Meanwhile the continuous buying suggested that he saw potential in Dempster, or he would cut loss swiftly like usual.

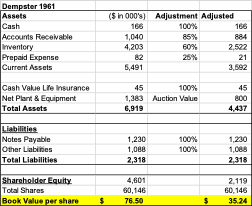

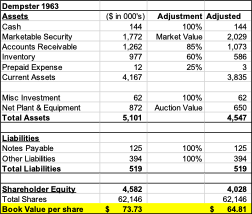

However, a closer look at Dempster’s 1961 balance sheet paints a troubling picture. The business had little cash. Over 75% of total assets were tied up in inventories and account receivables. The bank loan was almost 60% of the adjusted shareholder equity, an alarmingly high amount of leverage. In effect the business was illiquid.

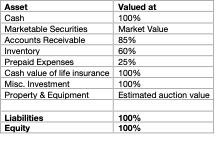

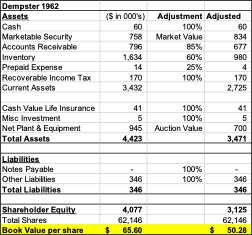

Given the challenges, Buffett valued Dempster conservatively as a going concern (liquidation mode). Liabilities were kept at face value, while assets like inventory and receivables were heavily discounted to reflect doubtful realization. This adjustment method brutally cut book value per share from $76 to $35. Ouch!

The message is clear. Unless assets convert to cash, their true value remains unknown. Accounting numbers can paint an incomplete picture. At an average purchase price of $28 the initial bargain now appeared much less attractive. A turnaround would be a monumental effort, but what did Buffett have in mind to revive the business and unlock its value?

Hiring Harry Bottle

In later years Buffett recounted that “Dempster was in big trouble under two previous managers, and the banks were treating us as a potential bankrupt [business].” After he took control, he replaced the management team. However, the new manager failed to reduce costs and continued to sink money into inventory, failing to meet Buffett’s expectation. In early 1962 the local bank was close to foreclose on the company inventory as collateral. At the same time any cost reduction bore real impact on the town’s economy, as Dempster was its major employer.

That was when Harry Bottle came to the rescue. Charlie Munger recommended Bottle, so Buffett quickly hired him with a $50,000 sign-on bonus. Buffett also threw in a 2,000-share option for Bottle, a 3% dilution. This aligned the incentives of Bottle and Buffett.

Prior to meeting Buffett, Harry Bottle worked at a business Munger had trouble operating. Bottle quickly gained expertise in distress turnaround situations. His skills in negotiations, cost-cutting (including the hard task of firing employees), and budgeting would play a big role in the Dempster turnaround.

Years later, Bottle recounted the experience as “I knew if we exerted the effort, we could turn it around and make it produce up to Warren's measure of performance - and that's pretty high”.

Bottle In Action

Harry Bottle took over the business with clear goals in mind:

Cut costs,

Clear out inventory,

Collect receivables from customer, and

Make use of the tax loss allowance, all to increase the liquidity of the business, so that Buffett could invest the cash the way he knew best.

In eighteen months, Harry Bottle surpassed all expectations and transformed Dempster into a lean, profitable machine. Buffett praised him “man of the year.”

Buffett wrote in his 1963 letter that

Our breakeven point has been cut virtually in half, slow-moving or dead merchandise has been sold or written off, marketing procedures have been revamped, and unprofitable facilities have been sold.

Inventory and receivables decreased by a staggering $2.8 million within six months, shrinking their overall percentage from 75% to 55% of total assets. The business paid off the bank loan and bought over $750,000 in securities. As a result, adjusted book value climbed from $35 to $50 per share.

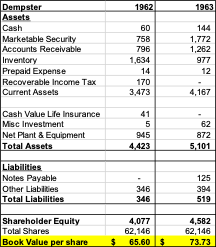

Bottle did even more to cut costs and sell down inventory in 1963. The inventory and receivable percentage further decreased to 44%. Adjusted book value further grew from $50 to $65 per share, much higher than $35 in 1961. The security portfolio alone was now worth more than Buffett’s purchase price.

This was no easy feat. The previous managers failed to make meaningful progress and the banks were treating the business as if it were already bankrupt. There are several key challenges involved in the turnaround. Firing people, slashing costs, and closing plants came with immense human cost. In the tight-knit rural community, many people’s livelihood depended on Dempster, making the reorganization painful. Over one hundred people lost their jobs.

Specific examples of Bottle’s actions include:

Drastically reducing inventory from $4 million in 1961 to $1 million in 1963.

Closed multiple factories and cut operating expense in half.

Raised prices of repair components in adaptable ways, bringing in additional revenue.

Freed up capital from the business for Buffett’s acquisition of securities.

Harry gave plenty of credit to Buffett and Munger for the price hike. He recounted in 2003:

One idea came from Warren and Charlie. Upon investigating our sales pricing structure, we were evaluating replacement and repair parts equal to the total of the sum of the completed item. So lacking any cost data to determine correct pricing, they suggested that we simply categorize all parts into three categories.

1. An item 100% proprietary, not available except from us. Increase up to 500%.

2. An item semi proprietary - Increase 200-300%.

3. Nonproprietary - Increase 0 to 100%.

We turned this inventory with an estimated inventory value of three hundred thousand into a resale value exceeding $2 million. Incidentally, we had few, if any, objections to our pricing strategy and continued to sell these parts at higher sales prices with little, if any, sales resistance.

This, of course, led us into other pricing updates and to support continued upward sales price adjustments. A cost data system was installed and maintained.

The insight was that pricing power may not be recognized and realized handily. For Dempster windmills, since owners will continue to use them, there is nowhere else to buy proprietary replacement parts. Because the equipment is used for extended periods of time, the higher cost can be spread out. The price hike for different types of parts is also adjusted to how irreplaceable they are, showing Buffett/Munger’s understanding of supply and demand.

Lessons From Dempster

Bottle’s fast turnaround quickly depleted Dempster’s tax loss. The business now had a lot of liquid assets. Buffett looked to sell the business to return the gains to his partners and minimize future taxes. A group of local businessmen bought the business at a book value of $80 per share, giving him a $2.3 million profit or almost three times his initial investment. Due to Dempster’s size in the partnership portfolio, its success helped to insulate the portfolio from market downturns. Buffett never lost money in any year in his 12-year partnership history. Harry Bottle’s stock option also provided him a nice performance bonus, which he invested in Buffett’s partnership and subsequently Berkshire Hathaway to great success.

Despite heavy criticism in the local community as a ruthless capitalist, Buffett’s ethical approach sold the new owner a much better business. He didn’t saddle the business with heavy debt and extracted all the value in the assets. Instead, he added value. Dempster is now profitable, lean, and robust.

Dempster’s turnaround success did many things for Buffett. He vowed never again to be labeled as a cold-blooded capitalist. Reputation became supremely important to him for the rest of his life. This directly influenced his decision to not to fire employees and keep Berkshire Hathaway in the textile business longer than he would like. It also set a clear blueprint for Berkshire Hathaway’s early years. As Buffett wrote in his 1963 letter, “we converted the assets from the manufacturing business, which has been a poor business, to a business which we think is a good business, [which is] securities.”

In his letters Buffett focused on Dempster’s business operations instead of its stock price. His framework on analyzing the balance sheet is still applicable today. He also noted the importance of buying cheap with a margin of safety. In this case, it was Dempster’s inventory, though its true value required an able manager like Bottle to unlock.

By buying assets at a bargain price, we don't need to pull any rabbits out of a hat to get extremely good percentage gains. This is the cornerstone of our investment philosophy: Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results.

However, we must acknowledge the counter factual. If it were not for Harry Bottle’s strong execution, Dempster would lose money or at best break even. Businesses in distress require incredible managerial talents, who set a sound strategy and execute regardless of the difficulties ahead. This inherent difficulty led Buffett in the following years to move away from cigar-butt investing to invest in high-quality business that come with great management. Regardless of a cheap price, if you cannot sell the windmills and reduce the inventories, you will continue to lose money and eventually go out of business.

In conclusion, the lessons from Dempster’s turnaround are as follows:

Dempster’s stock performance represents its underlying business.

The importance of capable and adaptable management.

The risk in investing in cigar-butts and turnaround situations, as management quality, execution, and intention are crucial.

Buy with a margin of safety, in this case buying below book value.

Being patient with accumulating shares, as well as waiting for business to improve.

Dempster’s story embodies the power of savvy investing, skilled management, and a commitment to ethical practices, offering valuable lessons for any investor.

Sources

For further reading on Dempster’s story, check out these sources. Thanks for reading!

Warren Buffett, Buffett Partnership Letters

Warren Buffett, Berkshire Hathaway Shareholder Letters

Alice Schroeder, The Snowball

Roger Lowenstein, Buffett: The Making of An American Capitalist

Disclaimer: Edited with help from Bard, a large language model by Google AI.

This was a great read! I have heard about Dempster Mill and Buffet before, but it the story was always about his public image, never really about the company and the incredible turnaround.